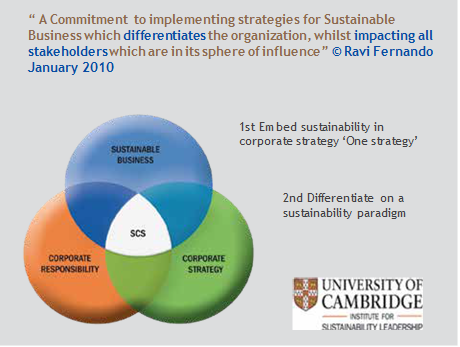

“Strategic Corporate Sustainability is not about how money is spent,it’s about how money is made”

Message from the

Chairman

of the Journal Commitee

2019 marks the 20th Anniversary of establishing Certified Management Accountants CMA”) of Sri Lanka the National Management Accounting body. Since then CMA Sri Lanka has come a long way in terms of recognition locally and globally in keeping with that,CMA Journal has achieved the status of

truly professional journal among the finance professionals and the business community.

This year the committee decided to focus on Sustainable Development Goals Agenda 2030-The Role of Professional Accountants”. Being Finance professionals we are

called upon to take more responsibility when it comes to our role in business sphere. In addition accountants are expected to take long term view rather than short term views in business which is not always the case.

CMA journal has been improved to a level to be one of the best journals in South Asia Region and our expectation is to achieve the level of being the best in Asian Region and we are confident of achieving that place in the coming years.

CMA Sri Lanka has provided opportunities for professional members to share their valuable experience in different business spheres by providing articles to the journal so that, other members will also benefit as whole.

The journal is for the members and we hope our members will contribute

more of their experience to the journal which will be an additional source of knowledge for our members.

I take this opportunity to thank Prof.Luxhman R Watawela founder President and President of CMA Sri Lanka for the guidance given to us,the council members and paper contributors and the staff of CMA

Sri Lanka for their unstinted support.

Adrian Perera

MBA(Sri J), FCCA, FCMA, FCMA(UK),

CGMA,FCPM and Asso.Member of Institute of Bankers of Sri Lanka

CERTIFIED MANAGEMENT ACCOUNTANT

Induction of CMA Sri Lanka President and Council Members 2019-2021

The fourth election to the council was held on the 9th May 2019. The new Act provided for a President, Vice President, three council members to be elected and three to be nominated by designated institutions from the Central Bank of Sri Lanka, Department of Accounting University of Sri Jayawardenapura and the Institute of Chartered Accountants of Sri Lanka.

The council of CMA Sri Lanka as per the incorporation Parliament Act No. 23 of 2009 for the year 2019 to 2021 are as follows:

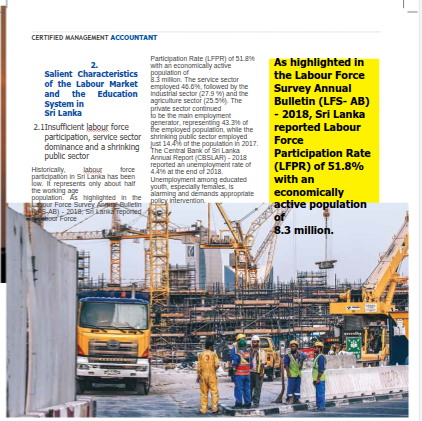

Prof. Lakshman R Watawala

President

Mr. Hennayake Mudiyanselage Hennayake Bandara

Vice President

Mr. Merrinnage Ruchira Asanka Perera

Council Member

Mr. Weerakoon Arachchige Adrian Damian Perera

Council Member

Mr. Jayasekera Mudiyanselage Udaya Bandara Jayasekera

Council Member

Mr. Manil Jayasinghe

Council Member

Mrs. Kumari Wijewardena

Council Member

Dr. Harendra Kariyawasam

Council Member

www.cma-srilanka.org | Volume 07 -No. 4 – September 2019 Page 9

CERTIFIED MANAGEMENT ACCOUNTANT

How do you define “Strategic Corporate

Sustainability”?

At the Outset, let me first share with you how the concept originated. Whilst reading for my Master’s Degree at Cambridge University, I focused on understanding ‘What makes some business embed sustainability in corporate strategy?’. It must be mentioned that under 3% of Business have actually done so. This led to a research study of all those UN Global Compact signatory companies in a National network to establish and identify ‘Common factors’ which set apart those companies which did so. This led to the concept of Strategic Corporate Sustainability -7 Imperatives for Sustainable biusiness’.

When ever the question of Sustainability strategy is posed to most business or National leaders, their response immediately migrates to CSR activities and how much money was spent on such activities as a % of the generated revenue or profit. This is an explanation of generated revenue or

Enlightened triple bottom line business leaders who are conversant with Strategic Corporate Sustainability know what matters is How money

is MADE? They focus on creating a ‘Sustainable profit generating business model, which does NOT impact the planet negatively, but contributes to social progress of people.’

www.cma-srilanka.org | Volume 07 -No. 4 – September 2019 Page 11

Strategic Corporate Sustainability, as defined below requires business to meet two non-negotiable criteria:

- The organization must embed Sustainability/Triple bottom line strategy in Corporate strategy.

- The organization will differentiate itself on a Sustaianbility led/triple bottom line paradigm.

The subject is comprehensively articulated in the publication shown below’.

Page 12 www.cma-srilanka.org | Volume 07 – No. 4 – September 2019

Extreme weather events 2

Failure of climate change mitigation & adaptation 4

Source: Global Risks Perception Survey 2017-2018, World Economics Forum

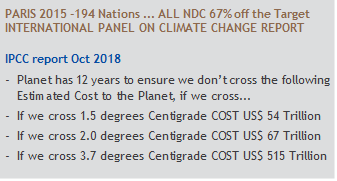

At the World Economic Forum ‘Risk Report’ 2017/2018, the above 5 risks were highlighted as being the ones to have the biggest impact on both nations and business in the next 10 years. 2028-2030! A closer examination confirms that Risk

2-3-4 & 5 all stem from Climate Change /Climate Emergency factors which are linked to the environment which is by and large as a result of human action. The majority of them are caused by the ‘unprecedented’ burining of fossil fuels (Coal, Petroleum, Diesel and natural gas) which has led to global warming with most nations recording the highest ever temperatures in 2000 years! In fact the past 19 years since the year 2000 are the ‘hottest’ ever recorded.

If one was to look closer at the end result of this unprecedented Global warming, the end result of burning fossil fuels is that global supply chains and end consumers are directly affected and will face the brunt of the Climate emergency in every nation of the planet unless we are able to urgently STOP burning fossil fuels and move 100% to renewable energy sources. The planet has heated up +1 degree centigrade from the average temperatures recorded in the pre industrial revolution 1880 period and set to cross between +1.5 Degrees to + 3.7 Degree Centigrade and the global crises of climate emergency and the associated losses to global GDP is captured in the IPCC (International Panel of Climate Change) in October 2018 as follows:

www.cma-srilanka.org | Volume 07 -No. 4 – September 2019 Page 13

Why should both Corporate and National Strategy focus on Climate

Emergency challenges?

The answer is clearly captured in the above slide which gives us the reality in terms of impact to both national and

business Supply Chains as sea levels rise and wipe them out. The fact is 98% of the planet is now affected by the Climate emergency, which leaves no nation or business that is isolated from the vulnerability of debilitating impacts.

Is there any impact of deforestation to the businesses and economy?

Every business Supply Chain will be affected in two ways if we continue with the deforestation we have so far inflicted on the planet where by 2018 we have wiped out over 70% of all our virgin forest cover /rain forests. This has also led to the destruction of over 60% of the planets fauna and flora species.

- It will seriously jeaprdize agriculture and raw material regeneration.

- It will impact the rain cycle to create massive droughts and water scarcity.

In the recent past we have seen South Africa and India declaring water crises in many of their key cities. Almost every nation will be affected by extream weather incidents of drought, extream teperatures and flooding as demonstrated in the slide below and if one studies it closely flooding, excessive rain fall and hurricanes acocund for over 70%

of extreme weather incidents which will having a drastic impact on all global supply chains and livelihood.

Extreme Weather incidents 1995-2015

- EXTREME TEMPERATURES

- DROUGHT & FOREST FIRES

- HURRICANES & FLOODS

Percentage of occurrences of natural disasters by disaster type (1995-2015)

Flood Storm Earthquake

Extreme temperature Landslide

Drought Wildfire

Volcanic activity

India is the most polluted country in the world and 22 of 30 most

polluted cities in the world are in India according to the CNN. Due to that is there any impact to Sri Lanka?

As we know, pollution does not need a visa to travel abroad and enter a nation. The sea and atmosphere carry a nations pollution across the sky and ocean. Sri Lanka is already seeing the impact in our sea shore of massive amounts

of plastic pollution ending up in our sea shore. As India increases its coal energy plants the ‘polluted’ air will be in our nation. The real crises will be when India runs out of water (already by July 2019 over 40% India is drought affected and Chennai declared a water emergency). Sri Lanka will face a geopolitical security threat as India runs out of fresh water.

Kandy district tops the list in air pollution in Sri Lanka. Its air is

polluted three times more than the air in Colombo. Is there any mechanism in

Sri Lanka to measure the air Pollution?

Unfortunately it is clear that ‘Air Pollution’ levels are NOT REPORTED as is the case in most nations. Widespread scientific air pollution monitoring and reporting is urgently required and it is surprising that both deforestation and air pollution don’t seem to be prirotiy issues at a National sustainability strategy level with over 86% of Sri Lankas’ virgin forest cover wiped out and the recent plans put

forward by the Ministry of Power and Reneweable energy to add 10 New Coal power plants when the one plant we have is having unprecedented health risks confirms that the nation is ignoring this risk.

Could you suggest few strategies we Can Reduce Our Reliance on Fossil

Fuels?

The Sri Lankan Government made a commitment at the UN Climate Change conference in Paris in December 2015

- To achieve 60% of all energy requirments with Renewable energy by 2020

- To achieve 80% of all energy requirments with Renewable energy by 2030

The recent CEB /Energy ministry presented strategy is to do the exact opposite with over 80% of our energy to be sourced by polluting fossil fuels by 2037.

The strategy available to Sri Lanka is clear if its committed to following the sustianble path.

- Pursue sustainable Solar/Battery and Wind energy soultions

- Accelerate Electric transportation for both public and private sector.

The sad reality is though New technology solutions in terms of Solar/Battery solutions available with Tesla & BYD (China) are already mobilized and working in South Australia, Hawaai, Costa Rica, Barbados to name a few recent cases the Government of Sri Lanka have ignored them to pursue a fossil fuel driven strategy which require Sri Lanka to exit the Paris agreement.

Any National Sutainable Development strategy needs to focus on the following 4 UN Sustainable Devleopment Goals and drive forward to achieve them without compromising them as is the case with fossil fuel driven energy today.

| 12 CONSUMPTION RESPONSIBLE | 15 ON LAND |

The four Key UNSDG led strategy is clearly articulated and urgently required to be mobilized in Sri Lanka. For an Advanced Strategic National Sustainability to be created

and mobilized in Sri Lanka, we need Sustainability mind set leaders. This is a perquisite…unfortunateky sadly lacking in the Nation today.

European countries vowed to ban diesel and petrol cars by 2040. Norway has

pledged to ban petrol and diesel vehicles by 2025, and India by 2030. What is your view on this?

As mentioned earlier the key reason for Global warming acceleration is the burning of fossil fuels for energy and transportation. This was confirmed in the recent July 2019 report presented by the Scientific community led by Dr Nathan Stieger of the University of Bern. Therefore any Nation remotely commited to avoiding the Climate emergency MUST move away rapidly from Fossil fuel

driven energy solutions and transport. In Sri Lanka, we are completely off the mark by actually increasing the Fossil fuel

/Coal driven energy solutions.

These advanced thinking Nations are moving in the right direction and will need to target 100% renewable energy driven transportation and energy solutions by 2030-2040! In order to achieve the above two major policy decsions are needed to BAN the importation of ‘New’ petrol and diesel

driven vehicles with immediate effect and to set up rapid charging electric networks in each nation. Ideally duyt free incentives for all Electric vehicle imports is also needed.

None of the above is happening in Sri Lanka today.

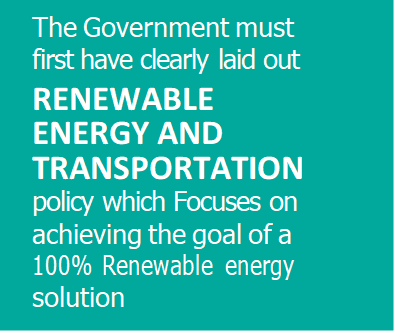

What is the role of government in renewable energy finance? Why would

the government invest in renewable energy?

The Government must first have clearly laid out RENEWABLE ENERGY AND TRANSPORTATION policy which Focuses on achieving the goal of a 100% Renewable energy solution.

Thereafter strategically tap into the latest Renewable energy technologies with globally available Sustainable enrgy supporting Climate Funding.

We should also work with the Chinese Asian Infrstructure Devleopment Bank, Asian Devleopment Bank, European Investment Bank to access funds to drive forward what is clearly the ONLY option we have committed to at the Paris Agreement.

As a key Nation in the China one belt , one road sea route we should learn from how Paksitan negotiatied with the Chinese Government to invest US$ 50 billion to completely modenrinze the nations energy sector from fossil fuels to Renewable energy. Sri Lanka has the bargaining power to do so.

Both physical and economic water shortages will threaten the very basis

of human life by 2015 according to the world resources institute water stress map.What are the strategies we can implement to overcome this problem?

I can categorially predict that the Key global conflicts from 2025 will almost certainly will be as a results of ‘Global water scarcity’.

The chart clearly demonstrates the crises faced by most Southern hemisphere nations where over 80% of the Worlds population resides.

While the World has only 3% of Fresh water for the needs of the every growing global popution, we have polluted over 70% of the fresh water and ground water available to mankind and ensured we jeapordize rain fall by wiping out over 70% of forest cover.

Could you briefly explain the Strategic Corporate Sustainability

imperatives for sustainable business?

The seven Imperatives identified are as follows:

The key strategies were already articulated in the above sections where we focused on 4 UNSDG’s. The Key focus SDG’s to drive the solution for the impending water crises are:

- Reforest with urgency with a manadatory 30% forest cover in every nation by 2030

- Harvest the Rain water and store with urgency for prolonged drought periods.

- De-pollute all the water ways and ground water

- Move to Prescision agriculture to save on the 70% of fresh water used in agriculture.

Page 16 www.cma-srilanka.org | Volume 07 – No. 4 – September 2019

How does strategic corporate sustainably impact to the triple

bottom line?

Strategic Corporate Sustiansbility is based on a business strategy that ensures ‘how money is made’ is through sustainable means. One key impact of it will strategically reduce both the impact and cost of all operations and increase the gross margin as a result.

Lower cost of energy, waste and water will immediately deliver savings.

CERTIFIED MANAGEMENT ACCOUNTANT

Do companies believe that sustainability -driven innovation

have the potential to bring business value to the organization?

Companies with a sustainability mind set leader not only believe but invest ONLY in Sustainability driven innovation. Tesla is an excellent example of this.

What is the importance of creating a sustainability culture in

the organization?

All Sustainbility mind set leaders will ensure that their organzations mainsteams sustainability/triple bottom line culture prevails in the organization as they know that they need every single member of the team and extended partners are of the same mind set to achieve its overall Corporate Strategy which is based on Strtageic Corporate sustainability.

A PERCEPTION OF THE ROLE OF A

FUTURE ACCOUNTANT

Abstract

CERTIFIED MANAGEMENT ACCOUNTANT

The purpose of this study is to analyze the perceptions of a future accountant’s role in business and to understand how education and the professional practice of accounting should change accordingly. This study comprised two hundred undergraduates from four different universities in Sri Lanka. The

areas of the study were leadership, ethics and professionalism. Exploratory and factor analysis were used to analyze the collected data. The findings of the study indicated that undergraduates perceive that accountants should have an above average level of professionalism, ethics and leadership. However, leadership has a negative relationship with ethics. The study suggests avenues for the profession to develop their image.

Introduction

Accountants will develop and sustain their personal and professional identities way beyond the definitions and images presented by professional associations and media. Failure to understand

this will affect the image of young professional accountants in the early years of their careers (Warren and Parker, 2009). A study by McDowall and Jackling in 2010 showed that Australian undergraduates perceived accounting

as rule-based and repetitive. This was a disturbing finding as this research

was done in an environment where the accounting curriculum has substantially changed within the last two decades.

The perception of accountants was however positive due to the promotional campaigns launched by professional accounting firms. A study conducted

by Jackling et al. revealed that ethical issues were likely to occur in accounting practices, which perceptions have been confirmed in current studies on the perception of accounting..

Dr. A. H. N. Kariyawasam Senior Lecturer, Department of Accounting, Faculty of Management Studies and Commerce, University of

Sri Jayewardenepura

It is important to study the perceptions of accounting in Sri Lanka in order, to understand how well the professional bodies could educate future accountants in keeping with what future managers want them to be. This will enable both professional and academic bodies to fashion [the ate their students better?] and to develop the accounting practice further. Accountants themselves will

be able to understand where their profession stands and what is expected of them from society. It is up to future accountants to shape their role in society and to change or develop the perceptions for the better.

A dynamic business environment requires accountants to change their mind set.

expected that through the findings of this study professional bodies will be able to change their curriculum accordingly so as to educate accountants to fit the needs of future businesses and to understand their future role. Professional and academic bodies will have to introduce extra-curricular activities designed

for their personality and leadership development. This research will also help to compare the roles of Sri Lankan accountants and those of other countries and how Sri Lankan accountants can fill the gap if they want to seek employment in other countries.

This paper consists of six sections. In the introduction the background and the aim of the study are explained. The available literature is discussed in the literature review. The methodology section explains the research approach, the sample, hypotheses, and variables. The data analysis section deals with the data analysis method and the results

section with the findings of the present study. The discussion section compares and contrasts the findings of the study with the available literature and the conclusion summarizes the findings and states the concluding remarks.

Literature Review

Perception of accountants According Joyce and Mun (2013), perceptions are intuitive first impressions, attributions and understandings relating to individuals and/or groups. This study focuses on the perceptions in respect of three aspects of a professional accountant in Sri Lanka, namely, leadership, ethical values and professionalism.

Leadership

Rehman and Naveed (2019) stated that leadership is the ability to motivate, influence and help others to contribute to a common goal. Leadership styles range from autocratic, participative, and laissez faire, according to Joyce and Mun, 2013, who explain leadership styles.

Autocratic leaders focus on control and management command. Financial controllers are traditionally expected to be highly rule-based, adopting an

autocratic leadership style. Participative leadership is based on team work and mutual exchange of ideas. Laissez faire leadership is a highly delegated approach that depends on the trust the leader places in his subordinates and with less interference.

In Joyce and Mun’s study, they state that, since management accountants are not bound by international financial

reporting standards as much as financial accountants, their role will extend

to planning, control and decision making functions, which require a certain amount of leadership. Further, management accountants have a duty to drive the organization through risk

mitigation and strategic planning, which involve risk analysis, risk management, internal control and maintenance.

Therefore, accountants should possess leadership qualities that enable them to lead organizations.

According to Deloo et al., 2011, the classic separation of “scorekeepers and business advisors” is slowly diminishing. Only business-oriented management accountants will be required in the future. They have also stated that even though scorekeeping activities are still

a prominent part of a management accountant’s day-to –day work, internal analysis and risk management also have become important in a management accountants’ work. Therefore, future

accountants are expected to contribute more through leadership than being

a mere scorekeeper. Management accountants will also witness a process of hybridization, where the accounting profession will be combined with another profession.

According to Craig and James (1993), International Financial Reporting Standards (IFRS) are modified to incorporate the dynamic information needs of organizations, industries and the public. Therefore, accountants in the profession should be able to embrace the change and be leaders of change to safeguard stakeholder interests. They should be transformational leaders

in the organization to better cater to the information requirements of stakeholders.

The accountant of the future is therefore required to have the above average leadership skills.

Ethics

As stated in Joyce and Mun’s study in 2013, Milton Friedman has stated that ethics maximizes the wealth of

shareholders. Therefore, an accountant’s ethical duty will be limited to adherence of regulations and providing information to enable shareholders to maximize their financial wealth. By adhering to these theories, an accountant will be only expected to monitor and control the efficiency of performance. However, this classical theory has been often critiqued for its exclusive focus on shareholders.

According to Pruzan (1998), accountants face ethical dilemmas just as any other professional. Ethical behavior cannot

be achieved purely through sound audit trails or recognized standards. There is an increasing need for ethical accounting and reporting to provide information

to external stakeholders and to protect corporate reputation. Value-based management will create productive organizational structures, systems of communication and measurements- evaluation reward systems, which can attract, hold and develop, intelligent, responsible, creative, independent and loyal employees. Therefore, accountants will be needed to adhere to value-based management so that ethical values will be expected from them.

Kranacher (2009) has stated that in order to create high quality reports, it is important that accountants hold values such as independence, accountability, integrity, and reliability. Being a profession, accounting requires its professionals to be ethical and maintain credibility through self-regulation.

This will ensure the exclusivity of the profession and social standards. A

rule-based system can be reactive to the environment, and will not be able to address all ethical issues fully. Therefore the accounting profession should be a moral community that is continuously engaged in ethical practices and makes its members understand the value of engaging in ethical practices.

Joyce and Mun in 2013 have found in their study that ethical values were negatively related to the role of accountants as leaders of change.

Students in Malaysia have perceived that engaging in ethical activities will be a hindrance to change. Love for money among accounting students was significantly related to unethical

behaviour. The above research shows that ethical values should be instilled at an early age as it takes time to develop. The negative perception on ethics contradicts the findings of e other studies mentioned previously.

Professionalism

A distinguished body that possesses a specific knowledge base and has the requisite expertise to further nurture

the development of the necessary skills [for the public?] will be recognized as a profession (Joyce and Mun, 2013).

Professions are also known for their integrity which is often a voluntary commitment through self-regulation.

Karanacher, 2009, has discussed whether accounting should be categorized as

an industry or as a profession. Since accountants are committed to holding specialized knowledge through extensive academic training and voluntarily involving increasing public interest, accounting can be categorized as a profession.

Traditionally accounting was perceived

as being limited to book keeping and primarily assumed administrative “bean counter” roles. According to Bloom and Myring, 2008, accountants are often depicted as negative and stereotypical. They also found that accountants should be more sensitive to culture and differences in behaviour and attitudes. The researchers found that there was a shortage of qualified accountants due to

the negative perception of the profession. According to Joyce and Mun, 2013,

the scandals of Enron and Worldcom in the USA and of Satyam in India have tarnished the credibility of the profession. To rebuild the reputation, accounting standards are moving from a rules- based approach to a

principles-based platform. The findings suggested that the sample selected for the study believed that accountants should demonstrate an above average level of professionalism. However,

the accounting profession has been stereotyped as boring and dull. To avoid this negative perception, Joyce and Mun have suggested that accountants should keep abreast of business developments and engage in meaningful CSR.

Methodology

Research approach

A quantitative study was carried out to seek the perceptions of future accountants, a deductive approach

for this research and a survey method to gather data from the sample with

a self-administered questionnaire. A similar method was adopted by Joyce and Mun, 2013 to analyze the perception of future accountants of Malaysian undergraduates. The questionnaire was in English to eliminate language barriers. The perceptions of future accountants were assumed to be measured by measuring their leadership, ethics and professionalism as mentioned above.

Variables

Joyce and Mun, 2013 chose leadership, ethics, and professionalism as variables to be measured so as to derive the perception of the role of a future accountant. Therefore, these variables were used in the Sri Lankan context as well. Indicators adopted for the above variables were as follows:

The reliability of the factors was tested using SPSS and Cronbach’s alpha resulting in 0.76 which is above the reliability threshold level of 0.7. These variables were used to discover the perceptions of a future accountant’s role through a five-point Likert scale.

Hypotheses

Based on the above variables, the following hypotheses were formulated. They hypotheses were tested through the collected data as the study follows a deductive approach:

H1-Future accountants would be expected to have a higher than average leadership score.

H2-Future accountants would be expected to have a higher than average score on ethical score.

H3-Future accountants would be expected to have a higher than average score on professionalism.

Population and sample

This study focused on seeking the perceptions about accountants of future managers, entrepreneurs and accountants, etc. The population

consisted of accounting undergraduates in Sri Lanka studying in local universities while considering the ease of data collection.

Data was collected from 200 accounting undergraduates chosen from, four different local universities based on convenience chosen at random to make sure the study was unbiased. A hardcopy questionnaire was distributed among the students as it was easier to administer and ensured a high response rate.

Participation in the study was voluntary and confidentiality was ensured.

Since it was a hardcopy questionnaire and the researcher was personally present at many of the data collection points, it was possible to collect 200 responses.

Data Collection

As mentioned earlier, a self-administered questionnaire was used to collect the data. The perceptions for each variable were collected through a five point Likert scale, 1=strongly disagree and

5= strongly agree. The questions were adapted from the study of Joyce and Mun, 2013.

Apart from the perception, demographic information was also collected from

the sample such as age, education level, and gender, etc. The collected data was [cleaned?] and manually entered into SPSS for analysis.

Analytical tools

The collected data was analyzed using SPSS version 25. Mean, median and mode tests were conducted to analyze the sample and its qualities. For analysis, Chronbach’s alpha, Bartlett’s test of spherecity, Regression, Standard Deviation, and Kaiser-Meyer-Olkin measure of sample adequacy were used.

These tests, inspired by the study of Joyce and Mun, 2013, were used to ascertain the generalized perception of future accountants.

Analysis

Descriptive statistics

The sample consisted of a majority (around 60%) of female students of the ages of 22-23, most of them following a professional course in accounting as well.

Factor analysis

Ethics, leadership and professionalism scored above 1 in Eigen values and therefore considered as valid factors. The KMO and Bartlett test score was 0.85 indicating suitability for factor analysis. Cronbach’s alpha value for the main study was 0.85 indicating a statistically reliable construct.

Professionalism was perceived to be more important for accountants than ethics and leadership as the means for professionalism was higher than that of the items in ethics and leadership.

Ethics had a negative relationship with leadership, as undergraduates who had ranked leadership highly marked low on ethics. However, it is not significant. Leadership and professionalism together have a significant influence on ethics.

Leadership has the highest explanatory power of 0.456 compared to the explanatory power of ethics of 0.078 and

0.231 for ethics.

Among the leadership qualities the highest mean was scored for personal attention. Honesty scored the highest in the ethics questions. Intelligence was deemed the most important quality of professionalism.

Discussion

The findings of this study will be useful to find what the businesses would want from their accountants in the future.

The respondents were generation Y,

who will be future business leaders. The undergraduate participants in the survey responded that they expect accountants to possess an above average level of leadership, ethics and professionalism.

This is an encouraging finding that helps to understand what qualities future accountants should possess.

Personally attending to financial matters is the most expected function of an accountant as leader, followed by recognizing and appreciating the efforts of others. This finding suggests that

an accountant should possess a more democratic or participative leadership style rather than an autocratic leadership style. It follows Joyce and Mun’s finding in 2013 that accountants’ leadership qualities are important. Deloo et. al’s

in 2011 predicted that accounting will face hybridization and accountants will have to work as business advisors. The findings of this study support the Deloo et. al’s finding that being a good communicator and being influential scored third and fourth places. Craig and James noted that accountants should be able to drive organizational change. The change element of this study has only scored a mean of 0.539 and gained 8th place in the ranking. However, the findings overall support the finding in the previous literature that accountants should possess above average leadership qualities.

Kranacher (2009) stated that accountants should possess values such as independence, accountability, integrity, and reliability and this study suggests that the highest perceived

ethical value of an accountant is honesty followed by trustworthiness. This follows Kranacher’s finding though the priority is different. Integrity has scored the lowest rank among the six ethical values. Pruzan (1998) arrived at a similar finding that accountants should show

value-based management and more ethical values. Ethical values have been ranked 5 by the respondents giving it lower priority compared to honesty and trustworthiness. Another interesting finding of this study was a negative relationship between leadership and ethical values, similar finding to Joyce and Mun (2013)’s finding. Students seem to think that ethical values will hinder good leadership qualities suggesting that students perceive ethical values have to be compromised in order to be a good leader who drives the organizational change. The result shows that extrinsic qualities are more valued than intrinsic qualities.

Professionalism is the second most important quality that an accountant should possess in the eyes of the undergraduates who participated

in this study. Being intelligent and knowledgeable are the two most important characteristics of an accountant as a professional. Bloom and Myring (2008) has stated that accountants should understand behavioral changes and cultural differences. Wisdom has been ranked below intelligence by Sri Lankan undergraduates. According to Joyce and Mun (2013), the reputation of accountants has declined due to

the Enron and Worldcom scandals. Adhering to professional standards has been ranked lowest in this study suggesting that Sri Lankan

undergraduates want accountants to use their skill more than blindly obeying the professional standards set by the

regulatory bodies. Probably this supports Deloo’s findings in 2011 as business oriented management accountants will be wanted by the organizations.

The findings of this study support most of the previous findings in the literature with minor deviations. All three factors

-leadership, ethics and professionalism- are important for future accountants.

Therefore, all three hypotheses are supported in this study.

Conclusion

According to the study, leadership and professionalism are expected to be instilled in the accountants to drive organizational change. Organizations will need to upgrade their training

programs so as to instill these values in accountants. Professional accountants will also need to assist their management by playing an instrumental role in risk management and also develop an ethical culture, without being limited to a passive role.

Accounting and business courses should be changed accordingly. Accounting professional institutes and academic bodies can research together and conduct frequent surveys so that future graduates will be better equipped to

face the changes in the environment. To increase professionalism and on- the-job leadership training, academics can be seconded for industrial training programs in banks, public accounting firms, manufacturing firms, etc.

Students should be encouraged to be critical about current issues across different business disciplines such

as marketing, operations, etc. Since accounting is multi faceted in nature this will ensure a more holistic approach and eliminate the perception of accountants as being dull and passive. Students can be encouraged to engage in peer discussions and to engage in rigorous research on ethics since it is not possible for rules to

cover all the loopholes in the accounting profession. Academics can act as mentors for students to sort out their ethical dilemmas.

Continuous Professional Development is a way to increase accountants’ professionalism. If accountants fail to display professionalism in their duties, it could affect the confidence level of shareholders and potential

investors. It is important that accounting practice maintain its ethical integrity and technical expertise as well as

professionalism in the public interest. As a profession is made up of individuals,

it is vital that the accounting profession and personal attributes are closely aligned.

Furthermore, business schools need to educate students to appreciate CSR. It needs to be included in the culture of business schools. This would promote greater application of how businesses and accounting disciplines can be combined to make a difference.

This research can be extended to accountants in practice and to different countries or could be done as a comparison between the perception

of accountants in practice and undergraduates.

References

- Bloom, R., & Myring, M. (2008). Charting the future of the accounting profession: Certified Public Accountant. The CPA Journal, 78(6), 65-67. Retrieved from http://ezproxy.uwl.ac.uk/

login?url=https://search.proquest.com/ docview/212236883?accountid=14769

- Craig, JamesL Jr., 1993, “A call for leadership: Certified Public

Accountant”, The CPA Journal, vol. 63, no. 7, pp. 16.

- Deloo, I., Verstegen, B., Swargamen, D., (2011) ‘Understanding the roles of management accountants’, European Business Review, 23(3), pp. 287-313 [Online]. Available at: https: // doi. org/10.1108/09555341111130263

(Accessed: 11th May, 2019).

- Jackling, B., Cooper, B., Leung, P., Dellaportas, S., (2007) ‘”Professional accounting bodies’ perceptions of ethical issues, causes of ethical failure and ethics education’, Managerial Auditing Journal, 22(9), pp. 928-944 [Online]. Available at:https://doi. org/10.1108/02686900710829426

(Accessed: 5th May, 2019).

Joyce K.H. Nga & Mun, S.W. 2013, “The perception of undergraduate students towards accountants and the role of accountants in driving organizational change: A case study of a Malaysian business school”, Education & Training, Vol. 55, No. 6,

www.cma-srilanka.org | Volume 07 -No. 4 – September 2019 Page 23

CERTIFIED MANAGEMENT ACCOUNTANT

Lalith Dhammika Mendis

FCA ACMA

Chief Executive Officer Helanta Communications (Pvt) Ltd

Fostering Quality Inclusive Education & Lifelong Learning to Drive Smart Inclusive Growth and Sustainable Development

Right to Education

The Universal Declaration of Human Rights adopted in 1948 recognizes education as a human right. Its Article 26 states, “Everyone has the right to education”. Although it is not a legally binding statement, it is globally accepted as a fundamental human right. Since its adoption, the right to education has been reaffirmed in numerous human rights treaties and declarations of the United Nations.

Sri Lankan Perspective Public spending on education as a percentage of GDP in Sri Lanka has been declining over the last four decades.

The education budget at 3.98% of GDP in 1967 declined to a modest 1.7% by 2012, despite a population increase from a little over 10 million in 1967 to over

20 million in 2012, a two-fold or 100% increase.

The end of an almost 30-year ethnic conflict in 2009 along with a so-called peace dividend was expected to lay the foundation for a revolutionary new beginning of socio-economic prosperity for the nation. Most of the socio- economic ills experienced during the period prior to 2009 were attributed to the ethnic conflict on the basis that it was drastically draining state coffers whilst negating any prospects of economic advancement. With the conflict becoming a thing of the past and peace restored, the economic whiz kids of successive political regimes set their eyes on making Sri Lanka the miracle of Asia. In economic terms, Sri Lanka was now aiming to become an “Upper Middle Income Nation”.

Inclusive Growth

Inclusive growth is a strategy designed to ensure the equitable sharing of economic benefits among all segments of society. It is a long-term perspective and entailing an approach whereby both microeconomic and macroeconomic determinants are aligned to the achievement of shared economic prosperity. It is ofcourse of fundamental

importance that detrimental externalities such as corruption are tackled to

ensure sustainable shared growth. In an inclusive growth approach, the pace and style of growth are interwoven because a rapid pace of growth is unarguably necessary for a speedy alleviation of poverty, while a broad-based pattern

of growth spanning all sectors of the economy and encompassing productive manpower ensures enduring shared growth in the long run. Realignment of public spending, design and execution of appropriate policies, provision

of motivational incentives to spur productivity and boost export revenues, and appropriate allocation of resources across the state machinery based on prudent economic principles catering to the needs of a “Upper Middle Income Nation” are vital for bridging the gap between where we are today and where we aspire to be within the target time horizon. In the economic thrust towards the desired goal, a vibrant private sector is expected to play a pivotal role in driving growth.

Crucial role of Knowledge and Innovation in Inclusive Growth

Knowledge and innovation are essential ingredients of “Smart Inclusive Growth”, which entails flagship initiatives to link education, enterprise, research and innovation. Modernizing manpower/ labour and developing new skills

and competencies are a fundamental requirement in this process. Knowledge is a vital ingredient of success and is fast becoming the dominant source

of economic progress in the “New International Economic Order”. In today’s context, more than a country’s land mass, natural resources or the availability of costly raw materials, or any other resource for that matter, the qualitative aspects of human capital in

terms of education, training, culture, competitiveness, technical knowhow and knowledge etc. are gaining more relevance for determining the economic strength of a nation.

Fostering human capital, the vital determinant of Smart Inclusive Growth

Fostering human capital has thus become an essential pre-requisite for economic growth. In the modern world, knowledge commands economic value. Hence for social and economic development and the competitiveness of a nation in terms of skills, knowledge and competencies in a dynamic global environment, the quality of human capital is of unparalleled importance.

To achieve inclusive growth to join the elite club of ‘Upper Middle Income Nations” in the global arena, the private sector is expected to play a dynamic and pivotal role ably assisted by the public sector, which is expected to handle

the required investments in upgrading infrastructure on a win-win basis. In order to drive business enterprises to achieve above average performance on a sustainable basis, the crucial importance of well-trained, skilled, techno-savvy and competent manpower with the right attitudes and ethics cannot be overemphasized.

However, it appears that the body politic has yet to realize that one of the most important drivers of a country’s growth is quality and inclusive education, the key to producing the right human capital. Unskilled manpower is simply basic labour. Skilled, competent and techno savvy labour forms human capital that drives the GDP of a nation. In

order to be competitive, forward-looking and in step with current developments, people need wide ranging qualifications and a multitude of skills and technical capabilities in a variety of disciplines.

In the fast emerging postmodern social order, knowledge-based organizations are assuming an unprecedented level of importance. Knowledge-based

economies appreciate the economic value of human knowledge as never before.

Globally accepted modern economic norms are placing growing emphasis on the need to recognize the value of human resources as an important component

of organizational assets. It is becoming evident that skills, qualifications and knowhow that enhance the quality

of human capital play a defining role in transforming information into productive knowledge that helps to create sustainable economic value. Hence, human capital that generates economic value becomes a major contributor to a country’s economic growth.

Table 1: Average Years of Schooling & Economic Development

Source: ADB economics working paper series 225

Human capital is an intangible asset. It is not disclosed in the typical Balance Sheet of a company. It can be defined as the sum total of the economic value of workers’ experience and skills to engage in productive activities that would generate income and surpluses for a company.

The Human Capital Theory recognizes that all manpower or labor would not be equal as each individual worker in an organization would not generate the same economic value. Economic value generated by each individual worker would not be equal. Productive

The average number of years of schooling in the world was reported as 8.12 years, with males having 8.41 years of schooling and females 7.84 years.

A person in an industrialized country has the longest period of schooling of 10.81 years, while a person in sub- Saharan Africa has an average of only

5.43 years. This is indicative of the crucial role of education in driving economic growth through productive human capital. Industrialized countries possess larger masses of human capital compared to developing or poor countries and

thus have the productive capacity to transform factors of production such as land, capital etc. into goods and services of economic value.

Public Spending on Quality, Inclusive Education – A Vital Investment

In this context expenditure incurred on quality inclusive education, no

doubt, is equivalent to an investment in human capital development, the reason being that productive capacity could be improved by the quality of education which, in turn, leads to enhanced skills, knowledge and competitiveness. It will also help cultivate important attributes that make human capital productive, innovative and efficient in contributing to economic success. It is evident that investing in human capital would lead to tangible returns in terms of higher national income and faster economic growth. Education can also lead to less crime and generate healthy habits in individuals from an early stage of their lives to help them grow

as responsible citizens contributing to socio economic development.

Accordingly, public spending on

Education is a vital investment with sustainable long-term benefits rather than an annually recurring expenditure. It would serve as a catalyst to boost national income and create “Economic Efficiency” through optimal use of scarce economic resources, which is enabled by improvements in the quality of human skills.

Education and Human Capital

What is Education?

Education encompasses structured institutionalized learning from kindergarten to university. It includes acquiring skills, widening knowledge and enriching experience beyond the typical classroom environment, such as social interaction, affinity with nature, use of media and the internet and engaging in practical activities designed to acquire and enhance competencies and knowledge as well as stimulate and sharpen cognitive development.

What is Human Capital? Human Capital has been defined in many ways. The Organisation for Economic Cooperation and

Development (OECD) defines it as “the knowledge, skills, competencies and other attributes embodied in individuals or groups of individuals acquired during their life and used to produce goods, services or ideas in market circumstances”.

Human Capital could also be considered the accumulation of knowledge, habits, social and personality attributes, including creativity and skills embodied in the ability to perform tasks designed to produce economic value.

skills, technical abilities, creativity and innovation would correspond to the education, training, attitudes,

innovativeness and the level of skills of an individual worker.

Role of education in building Human Capital

Human Capital consists of four basic components; skills, capabilities, knowledge and personal attributes such as creativity, innovativeness, right attitude, commitment to achieve goals, loyalty, trustworthiness, integrity, etc. and therefore can be broadly classified into two main categories: Acquired Human Capital and Inborn Human Capital

Natural abilities and attributes help to differentiate and make a person unique. Such attributes cannot be acquired or transferred to others. For example, Albert Einstein’s creative thinking ability was unique to him. Similarly, one could become a good singer due to the natural gift of a melodious voice.

Acquired human capital, such as skills and capabilities could always be gained by individuals through training and engaging in various activities designed to enhance and sharpen skills and expand knowledge. An organization could improve human capital by investing in training programmes to develop specific job related skills.

Employees with superior skills, higher qualifications and capabilities are more highly remunerated than others, demonstrating the economic value of Human Capital.

Education enriches Human Capital and helps people make decisions for the benefit of society as a whole. A well- educated person could be expected to desist from socially objectionable and detrimental behavior and contribute

to the advancement of society. Education paves the way to reducing criminal behavior and cultivating socially responsible habits, mannerisms and ethical conduct leading to socio economic progress. The educated strata are better informed about continuously evolving global trends in socio-economic development and modern technology that contribute to changing every aspect of human existence. Education promotes wholesome habits, imparts knowledge, guides people to adopt healthy life styles and desist from morally objectionable and socially detrimental activities that would result in a substantial reduction of unproductive social costs that will enable public money to be diverted to worthy causes for the sustainable advancement of society.

For education to effectively build Human Capital, it has to be inclusive and non- discriminatory, enabling each layer of the social hierarchy to benefit from it. This will enable a mass creation of Human Capital that would lead to GDP growth.

Human Capital and Economic Growth

Robert Solow’s Neo Classical Theory of Economic Growth recognizes Education as a key determinant of economic growth. Although education per se was not a direct factor in his growth theory, his model provided the impetus for focusing on education on the basis that an educated population

representing human capital is necessary for technological innovation.

Nelson and Phelps explained “investment in humans”: workers needed education in order to use new technologies, thereby increasing total factor productivity and spurring economic growth. Later, endogenous growth models propounded by Lucas

(1988); Romer; Barro and Sala-i-Martin demonstrated that the accumulation of human capital through education and on-the-job training fosters economic

growth by improving labour productivity, promoting technological innovation and adaptation.

Human capital and economic growth are closely related: human capital can help to develop an economy through the knowledge and skills of people. It refers to the knowledge, skill sets and motivation of people which provide economic value. The concept of human capital means that everyone does not have the same skill sets or knowledge bases and the quality of work can

be improved by investing in people’s education.

Economic growth implies an increase in an economy’s ability, compared to past periods, to produce goods and services with greater economic value. It can be determined by measuring the change in the real gross domestic product (GDP) of a country. How Human Capital and Economic Growth are related and can

be measured by how much is invested in people’s education. For example, many governments offer higher education

free to people because they realize that the knowledge people gain through education helps develop an economy leading to economic growth. Workers with more education tend to have higher earnings, which then increases economic growth through additional spending.

Growth Prospects offered by Globalisation/ Global Value Chains

Globalization offers new and greater opportunities in the trade of goods and services to the developing world. Advancements in the ICT sector has enabled Global Value Chains to effect physical fragmentation of production processes by geographically dispersing the activities over preferred locations based on efficiency and low cost

considerations. This involves outsourcing as well as off-shoring. For a country to

be a part of a global/regional value chain it has to have infrastructure, education, rule of law and a good standard of health. Globalization has contributed to the development of the education systems in developing countries. We can clearly see that access to education has increased

in recent years as globalization offers a catalyst to jobs that require higher skills set. This demand has driven people to pursue higher levels of education and enhance their skills so as to enjoy better employment opportunities.

Common features of economic transformation influenced by Global Value Chains

- Export orientation focused on manufactured goods;

- Adaptation to ever “higher added- value” activity;

- High levels of investment and savings;

- Increases in rural productivity;

- Increases in income equality;

- Adaptation to the information paradigm;

- Availability of educated, low-paid, highly productive and disciplined labour;

- High levels of basic education and literacy for economic growth;

- Gender-equitable access;

- Equitable public education expenditure; and,

- Open, competitive and largely meritocratic education.

With G20 countries assuming greater economic weight in the Global Value Chain, Sri Lanka has to evolve forward looking policy measures to reform its education system to produce the high level skills required by a rapidly evolving knowledge economy. This will enable Sri Lanka to compete with regional players to secure opportunities at the higher levels of regional/value chains that offer greater economic benefits.

Strategic initiatives will be required to objectively study and implement necessary reforms in the present education system so that it will be

relevant to globally evolving trends and the opportunities offered by regional/ global value chains.

It is essential that reforms be introduced as early as from the kindergarten. Pre- school education plays a pivotal role

in the socialization of children from an early age. Primary and secondary education should provide inclusive

access to quality education that enables students to acquire essential basic skills and key competences relevant to a fast evolving knowledge economy marked by stiff competition. Methodologies should be established to ensure purpose- driven differentiation whereby children are categorized into sub groups based

on skills and abilities at Grade 11/12 pre-university level. Safeguards may be

required to avoid inequality, especially with regard to the disadvantaged. “The Knowledge Triangle”, the interaction between Education, Research and Innovation, is the key driver of

a knowledge-based society. “The Knowledge Triangle” is the key to the advancement of a knowledge-based economy and society.

Lifelong Learning

Lifelong learning is the process of continuing to learn new skills, enhance knowledge and acquire competencies on an ongoing basis throughout a person’s life. Successful people tend to have better reading habits, attend conventions and participate in various programmes that offer new insights that help them become more effective in their chosen fields.

There are three different kinds of lifelong education:

- Maintenance Learning – being up to date in your chosen field.

- Growth Learning – learning that adds novel knowledge and skills to those an individual already possesses.

- Shock Learning – learning that contradicts or reverses a piece of knowledge or understanding that an individual already has.

Lifelong Learning and the Challenges of an Aging Population

The Sri Lankan population is rapidly

ageing. Demographic statistics indicate that the Sri Lankan population in

2012 above the age of 60 years was 2.5 million, which was 12.5% of the total population. The number is projected to increase to 3.6 million or 16.7% of the total population by 2021. By 2041, it is expected to further increase to one- quarter of the population. This indicates that Sri Lanka’s Dependency Ratio

is on the rise. The challenges arising from an aging population are several. It causes a strain on public financing in the form of public funded pension

payments and allocation of funds to fulfil elderly health care and welfare needs. A shrinking labour force resulting from a short supply of young talent and a greater portion of the population in retirement will negatively affect national output. In Sri Lanka elderly people very often lead active lives and as a result many prefer to remain in the workforce

even after retirement. Therefore, the Government could explore the

possibility of implementing appropriate policy measures to retain people over 60 years in the active labour force. One of the options would be to redefine the age of retirement.

The Government could initiate policy measures to provide continuous learning

opportunities for senior citizens

to enable them to further widen their knowledge and sharpen their skills in productive activities. Those that remain active even after reaching the age of retirement would naturally enjoy better health and be psychologically strong to grapple with age-related issues. They could with enhanced skills and newly acquired capabilities enjoy better quality lifestyles and continue to support themselves without being a financial burden. There could even be industries and service sectors where senior citizen could still

provide constructive contributions based on their longstanding experience and continuous learning.

Conclusion

Sri Lanka could emulate the success story of countries that have risen (for example, Singapore) through building a progressive and forward looking educational system characterized by meritocracy and equal opportunities.

Education should be given pride of place as one of the key drivers of

smart inclusive growth and sustainable development.

Q. What are the first steps of a waste

management programme in our context?

Starting with waste profiling and identifying the exact content of waste (chemical/physical parameters) the internal approval process comprises of technical, environmental safety and health, and financial feasibility of meeting the waste disposal need.

Being the only party who has the license for [haz/hazardous] waste transport, storing and disposal we submit a comprehensive proposal to the customer.

Once the customer agrees with all the conditions we undertake the final disposal. During the delivery there is a verification process to check whether

the same approved material is actually delivered.

Once disposal is completed, we issue the thermal destruction certificate.

Q. What is Ecocycle Lanka and what is their main

role in conducting sound waste management practices and its commitment to sustainable development?

INSEE Ecocycle, the sustainable waste management arm of the country’s premier cement manufacturer INSEE Cement, provides sustainable waste management solutions that would make a significant difference from a national perspective. INSEE Ecocycle has been in the waste management industry for almost 16 years sharing its expertise knowledge, globally accepted technologies and management commitment as the most preferred waste management service provider in the country.

INSEE Ecocycle is the only comprehensive industrial waste management solutions provider in Sri Lanka with an annual capacity of

100,000 MT providing environmentally friendly industrial solutions to public and private institutions especially

for managing hazardous waste. We have currently invested Rs. 1.3 bn to provide solutions for 700 industries covering government, multinational and other local conglomerates.

With the current expansion, the company will make a greater contribution to national waste management, with the world-class resources of its parent company INSEE Ecocyclye in Thailand specializing

in industrial solutions in the region. The newly added service, the “INSEE Ecocycle Environment Solutions” arm includes services such as laboratory services, training and consultancy,

industrial cleaning, specialized logistics service environmental remediation, emergency response services, e-waste disposal, etc.

Q. What is their main operation hub and

what kind of facilities do they provide?

The main operation hub is the Katunayake pre- processing facility located at KEPZ,

laboratory services for waste analysis and specialized logistics for transporting and storing waste.

Q. What kind of technology is currently

used at Ecocycle Lanka?

Co-processing

Q. What is the difference between co-processing

and pre-processing?

Co-processing

Co- processing is a unique industrial process offered for the proper management of industrial waste through thermal destruction. It is a combination of the two processes of clinker manufacturing and industrial waste disposal, both carried out in the same environment as a single combined operation without adverse effects on each other.

Pre-Processing

We can’t dispose of all the waste as it is using a cement kiln. We must do some chemical and physical treatment to wastes prior to final disposal through co-processing. This is called the Pre- processing operation and it is done at our Katunayake pre-processing facility.

Q. What’s the difference between “co-

processing of waste in cement kiln” and “incineration”?

Co-processing is a globally accepted sustainable waste management technique which is also considered

a thermal treatment method and it completely destroys the waste

material. Energy generated for cement manufacturing is used to destroy

the waste with suitable resource utilization.

Incineration is also a thermal waste treatment process that converts the waste material into ash, flue gas and heat. It has a low temperature

compared to co- processing and the waste materials are not destroyed but the final residue is disposed of

properly. Additional energy is need for the system to destroy waste materials.

Do your preprocessing and coprocessing

facilities follow the regulatory technical standards and license?

Pre- Processing Facility

- Central Environment Authority schedule waste management licence,

- Central Environment Authority environmental protection licence, and

- Katunayake Export Processing Zone

-BOI environmental protection licence.

Co-processing Facility

- Central Environment Authority scheduled waste management licence,

What are the environmental

benefits of co-processing, co-processing to companies and co-processing to communities?

For the environment:

- Lowers CO2 intensity from facilities that use co- processed waste as fuel,

- Reduces CO2 emissions from burning waste which cannot be recycled,

- Reduces methane from landfills, and

- Conserves natural resources.

For Companies:

- Ensures complete thermal destruction of waste, and

- Reduces liability and risk to corporate reputation, enables

Is your company involved in e waste

disposal?

Yes, we provide environmentally friendly disposal solutions for e- waste. We assure zero footprint.

We are the first to introduce special disposal solutions for printer toner cartridges.

What is Insee’s contribution to

reducing the co2 footprint?

Following the saved CO2 footprint from the beginning and responsibly disposing of waste materials.

Waste vol Co-processed in Mts

- Provincial Environment Authority scheduled waste management licence,

- Central Environment Authority environmental protection licence, and

- Provincial Environment Authority environmental protection licence.

enhanced your regulatory compliance.

For Communities:

- Reduces the amount of raw waste going to open dumps,

- Conserves energy sources for the future, generations, and

- Creates job opportunities.

CO2 saving in Mts

2003-2006 2007-2010

322,367

2011-2014 2015-2018

Q. INSEE Ecocycle provides environmental

solutions to Sri Lanka’s municipal solid waste crisis through public private partnership. What is your relationship with the government and environment- related regulators such as

the Central Environmental Authority?

While island-wide Municipal Councils are struggling with challenges associated with waste disposal and recycling, INSEE Ecocycle, the waste management arm of INSEE Cement, has spearheaded a well-structured Public-Private Partnership (PPP) for Municipal Solid Waste management in co-processing “segregated non- recyclable plastic, polythene waste

from MSW’ since 2012 in Gampaha and Kurunegala districts.

As a pioneering initiative, the partnership has successfully demonstrated how the combined strengths of proactive private entities, the Central Environmental Authority,

Q. Insee Cement has won the National Green

Awards in Sri Lanka several times and adheres to eco- friendly waste management practices maintained by Insee Ecocycle. What can you say about this?

Bureau (PNB) and National Dangerous Drugs Control Board (NDDCB) to responsibly dispose of 928 kg of waste cocaine hydrochloride through cement kiln co-processing for the first time in Sri Lanka.

Q. How many corporates including government

institutions are closely working with Insee Ecocycle on industrial waste disposal?

About 700 + corporates work with us -mainly corporate, multinational companies, local conglomerates and government organizations.

Q. Does Insee Ecocycle assist in disposing

of chemical waste from laboratories?

Yes, Ecocycle accepts chemical waste from laboratories and we have already recommended a solution to the Registrar of Pesticides, University of Peradeniya, etc.

CERTIFIED MANAGEMENT ACCOUNTANT

How do you educate the younger generation on sustainability concepts and waste management?

Does Insee conduct awareness programmes on sustainability concepts and waste management in Sri Lankan schools?

INSEE is continuously working with schools [which are in its facilities communities?]

INSEE Ecocycle has signed an MOU with the University of Sri Jayewardenepura and Sri Lanka Association of Australia Awards Alumni (SLAAAA) on institutional collaboration to conduct awareness programmes on sustainability concepts and waste management in Sri Lankan schools

How does the INSEE family support the national drugs prevention programme?

It helped In cocaine disposal on two occasions.

Page 34 www.cma-srilanka.org | Volume 07 – No. 4 – September 2019

CERTIFIED MANAGEMENT ACCOUNTANT

A PERSPECTIVE ON BUILDING A SUSTAINABLE

ANTI-MONEY LAUNDERING

ENVIRONMENT AMIDST EVOLVING TECHNOLOGIES OF

CRYPTO ASSETS AND BLOCKCHAIN

- Introduction

Money Laundering is a global threat requiring the urgent attention of policy makers to protect financial systems from criminals. Rapid developments in financial innovation, information technology and communication processes have paved the way for money to move anywhere in the world with speed and ease, making the task of combating money laundering an even more daunting task. The United Nation’s Office on Drugs and Crime (UNODC) (2019) estimates that the

amount of money laundered globally in a particular year ranges from around

2-5% of global GDP or US$ 800 billion to US$ 2 trillion in current US dollar terms. McDowell (2001) defines money laundering as the act of channeling illicit funds through outside financial

channels in order to make funds appear legitimate. According to FATF(2019), money laundering is the processing

of criminal proceeds to disguise their illegal origin. The main motive of money laundering is to disguise the source of assets in order to avoid detection of the illegal activity from which the assets were derived. The intent of the criminal is to conceal, safeguard and use the illicit proceeds at a future date when the “heat” has sufficiently died down in searching for the money and the criminal. This

is summarized by UNODC(2019)

as criminals trying to launder money to hide evidence of the money trail

of their crimes. Further, money itself is vulnerable to seizure and has to be protected .

A typical money laundering cycle consists of a dynamic three-stage process: placement, layering and integration, regardless of who uses the apparatus

of money laundering. At the first stage, criminals enter the “dirty money” in the

financial system. At the second stage, they perform a series of transactions to conceal the origin of the funds, which include breaking the funds into much less conspicuous levels and layering so that the lesser amounts are not easy to

Figure-1: A Typical Money Laundering Process

detect. At the final stage of integration, funds which were broken up into smaller portions are integrated into the economy appearing as legitimately earned/ speculated/invested funds. This process is further clarified in Figure-1.

that needs the relevant jurisdictions to strengthen their domestic legal frameworks and take other measures to safeguard financial systems and economies from criminals.

This, however, is not an easy process due to the continuous innovations in financial technology, the rapid

evolution of Information Technology such as block chain and internet- based payment methods like crypto

currencies. Although these are relatively new areas, crypto currencies enabled

by block chain technology are easily accessible to criminal elements as a tool in the process of covering up the illicit origins of criminal proceeds. For example, McCahill (2019) reports that a terrorist organisation had converted cryptocurrency into physical currency shortly before carrying out the deadly Easter Sunday suicide attacks at several

locations in Sri Lanka on April 21, 2019. While this remains the background to this paper, the discussion will address the implications of evolved technology, especially Blockchain technology and cryptocurrencies, on criminal elements relating to money laundering.

Cryptocurrencies are becoming popular, creating a new payment platform which challenges traditional banking. A crypto asset has come a long way since its inception as an alternate form of currency or payment that did not require third party intervention. Nakamoto(2008) first introduced cryptocurrencies by

publishing an email in the Cryptography Mailing List, stating simply, “I’ve been working on a new electronic cash system that’s fully peer-to-peer, with no trusted third party”. He published a white paper outlining a peer-to-peer electronic cash system called “Bitcoin”. Even though

the crypto asset system appears to be complex, its operational mechanism is easy to understand. The main purpose of developing an electronic cash system was to allow online payments from one party to another without going through a financial institution. This electronic cash system will eliminate the costs

of transactions such as commissions and fees and the payments would be authorized through a system of digital signatures. The need for having a bank

parties involved would be obviated by establishing a network system. So, the trust to be established by the presence of a financial institution would be built through cryptographic proof.

Transactions are grouped into blocks and time stamped for easy verification of payments. Double payments are prevented through timestamping. Peers are organized as networks to avoid

third-party intervention and facilities are provided to combine or split payments.

An electronic coin, the primary unit of a transaction, is a chain of digital signatures. Each owner possesses two keys, a public key that can be seen by

others and a private key known only to him, generated by the computer system. Coins are transferred by the present owner to another by signing a hash,

an authentication that it is a genuine transfer from the previous owner and the public key of the next owner while simultaneously authorizing the transfer by signing his private key. The coins are stored in a digital wallet and the use of the public key and private key will enable the new owner to open his wallet and release the coins stored therein. Thus,

there is a chain of all transfers made with all transfers connected through a node,

a point at which two digital signatures

meet. The new owner can verify the authenticity of the transfer by looking into the public keys of all the previous

transfers. The work of Nakamoto (2008) is now known as Blockchain technology and depicted as follows:

The development of crypto currencies challenges the status quo of well- established financial institutions with the additional risk of emerging technology being used for illegal activities. The

Basel Committee (2018) states that while the crypto-asset market remains small relative to that of the global financial system, and banks currently have minimal direct exposure, the continued growth of crypto-asset trading platforms and new commercial products related to crypto-assets have the potential to raise financial stability concerns and increase risks faced by banks. In this context, recent and expected future developments of crypto assets will be important to strengthen the efforts of a jurisdiction’s

anti-money laundering laws to counter the financing of terrorism.

- Using crypto assets to cleanse illicit proceeds of crime

Although this is a relatively new area, many have delved into the detailed incidents of crypto assets being used by criminals as a process of covering up the illicit origins of the proceeds of crime (McCahill, 2019). A number of high profile investigations and prosecutions suggest Bitcoin to be the most sought after choice of currency for criminals (Malik, 2018). Bitcoin has been used in the buying and selling of illegal drugs, purchasing internet malware bots and

spying tools in dark web sites, laundering funds through online games and funding acts of terrorism.

Bitcoin’s popularity has increased its mining activity and circulation. The Bitcoin blockchain is a public ledger of all

Bitcoin transactions that have been executed. It is constantly growing as ‘completed’ blocks are added to it with a new set of recordings. The blocks are added to the blockchain in a linear, chronological order. Thus far, the number of Bitcoins has been growing

since the creation of this virtual currency in 2009 reaching approximately 17.12 million in June 2018. A typical money

laundering process would have a money laundering cycle, which involves placement, layering and integration. A

typical process using crypto assets would also follow these three steps as follows:

Step 1: Placement

The criminal purchases a basic crypto asset at a digital exchange using illicit proceeds (cash, digital currency, or debit/ credit/ATM card). Crypto asset exchange service providers are usually obligated by law to conduct customer due diligence measures. These digital exchanges

would often be accessed by straw men working and posing as a front for known criminals and criminal networks. A straw man /men may provide a degree of anonymity to the criminals and criminal networks. Anonymity is extended by using Virtual Private Networks (VPN), anonymous e-wallets and blockchain enabled smartphones. At the placement stage, once the initial identification, verification and KYC is done, the digital

exchange will transact fiat currency or bank transfers to place funds to