Introduction

Supplier risk management is in flux. While supply chain leaders have readjusted to business as usual following the Covid-19 pandemic, there is no doubt that it exposed global supply chains’ fragility. In addition to seismic disruptions and production delays, demand for some products soared, leaving suppliers struggling to keep pace. The immediate steps taken to mitigate these risks were not only chaotic for supply chain leaders but also costly, as stockpiling inventory or scrambling for alternative suppliers became an all-too-familiar approach.

It is no wonder, now with the dust firmly settled, that many firms are rethinking and rebuilding their approach to supplier risk management so it not only advances

resilience but is also more cost-conscious. And time is certainly of the essence. Evidence points to similar disruptions only becoming more common and severe, as recently seen following the rising geopolitical tensions and wars in the Middle East and Ukraine. It is paramount that supply chain teams are able to respond to disruption while protecting revenue and controlling costs.

THIS EBOOK WILL EXPLORE

→ The concept of VaR, how it is measured, and how it can be applied to supply chain management

→ The importance of enterprise data and predictive analytics to inform reliable VaR calculations

→ Real-world examples detailing how VaR can be applied in practice

From data to decisions: why using value at risk calculations can bolster supply chain management 1

SUPPLY CHAIN RISKS:

AN OVERVIEW

In short, the pandemic produced a real- life lesson that proactive supply chain risk

management can be less costly than reactive approaches. The question then becomes what can be done?

Against this complex backdrop, Moody’s believes there are levers at the supply chain team’s disposal that can help. Among them is the application of value at risk (VaR).

While more commonly used in financial modeling, VaR is not necessarily new to supplier risk management. It provides a more objective measurement of how risk mitigation strategies protect revenue — enabling supplier risk professionals to make more targeted, data- and outcome-led supply chain decisions according to the outcome or value a risk mitigation response can achieve.

But there’s no doubt that VaR among supply chain professionals is resurfacing, and the reason why is clear: The greater quality and availability of enterprise data today means that VaR calculations are more reliable and

can therefore become the cornerstone of a corporate’s supplier risk strategy.

It has the potential to empower supply chain professionals to better communicate their actions, decisions, and outcomes to senior management. VaR can certainly play a fundamental role in this respect: Supply chain teams can apply it to more confidently communicate risk mitigation strategies to boards during times of crisis.

Central to VaR’s efficacy is the availability of sophisticated enterprise-level data.

Thankfully, supply chain leaders today have access to an abundance of resources and analytics that ensure they shift from reactive and after-the-fact mitigation strategies to forward-looking and proactive approaches.

With the non-targeted approach to supply chain risk management now a thing of the past, this paper will explain the critical role VaR can play in helping supply chain

leaders understand the efficacy of their risk mitigation strategies. It will also provide real- world examples of how VaR can be practically applied to help maintain supply chain performance and resilience.

The key questions

that value at risk answers:

→ What is the supply chain team protecting as its key objective — revenue, the guaranteed supply of goods, timely delivery?

→ In the event of disruption, what could be lost?

→ Based on how much it would cost the company to avoid these losses, is the cost of the mitigation a sound investment?

At its core, value at risk is an expression of the number of days a firm can continue to supply a

generate revenue — before a disruption could lead to tangible losses due to the nonfulfilment of an order.

Value is not always revenue

To give an example, we can look at value at risk being applied to two scenarios at a fictitious company:

SCENARIO 1

Company A supplies an electronic component that generates daily revenue of $100,000. The company currently has 10 days of inventory based on existing orders and projected sales and a recovery time of 20 days.

The risk exposure index for this product can be calculated as follows:

$100,000 x (20 – 10) = $1 million

The probability of disruption can be based on historical data, expert judgment, or scenario analysis. For simplicity, let’s assume that

the supply chain leader uses historical data and predictive analytics to estimate the probability of disruption to be 10%. The value at risk for this product is:

$1 million x 10% = $100,000

This means if a disruption occurs, Company A has $100,000 in revenue at risk for this

product. By comparing the value at risk across different products, the supply chain leader can prioritize the most critical products to protect by using mitigation strategies accordingly.

SCENARIO 2

Company A supplies a second component that also generates daily revenue of $100,000. It only has five days of inventory and a recovery time of 20 days.

In this scenario, the company identifies that there is a 70% chance that its supplier is at risk of not fulfilling its commitments. In the event of disruption, for each day that orders are not fulfilled, the company will miss out on

$100,000 in revenue each day for 15 days (or

$1.5 million total). Since the probability is 70%, the value at risk is $1.05 million, if calculated at that particular confidence level.

Faced with these two scenarios simultaneously, the supply chain leader can reasonably approach the board and request resources to intervene in order to protect a larger proportion of the revenue that could be lost. As such, the keys to effective supply chain management are understanding which

risks must be mitigated as a priority, what the cost of inaction is, and, most importantly, a crystal-clear view on the true value of what risk mitigation strategies are attempting

to protect.

Value at risk:

the key benefits

REVENUE-BASED DECISION-MAKING

VaR calculations can help justify risk mitigation strategies by clearly outlining the costs as well as the anticipated revenue that can be protected, aiding supply chain leaders to make better decisions according to their risk profiles.

EASING BOARD ENGAGEMENT

VaR introduces a more transparent measure of anticipated return of investment, not only easing conversations around the cost-benefits

of near-term risk mitigation strategies but also in demonstrating the longer-term value of investment in the supplier risk management function.

RISK PRIORITIZATION

Using a VaR calculation, the suppliers that expose a firm to heightened revenue risk can be identified and assessed more easily. By thinking about supply chain risks with a revenue-first mindset, supply chain leaders can make better decisions that avoid mitigating risks that do not pose the greatest threat to revenues.

IMPROVED RESILIENCE

Supply chain resilience is the capacity to absorb, mitigate, and avoid shocks to the supply chain. By calculating VaR, supply chain professionals

can ensure that the largest and most severe anticipated shocks to the supply are prioritized, absorbed, and lessened.

COMMUNICATING IMPACT

In recent years, the supply chain function has transitioned from being a reactive cost center to one that is expected to proactively maximize revenue.

VaR enables supply chain professionals to clearly demonstrate the value the function brings to a company’s bottom line.

The concept can also help alleviate a secondary issue in the supply chain field: professional attrition and high turnover rates. In recent years, we’ve noted higher levels of employee

dissatisfaction among supply chain professionals. In a 2023 Gartner survey, 93% of respondents said burnout-related turnover had increased at

their organization1.

We see VaR as a possible antidote to help these professionals better demonstrate value to employers, which in turn can lead to greater employee engagement and satisfaction.

1 https://www.gartner.com/peer-community/

oneminuteinsights/managing-burnout-during-supply- chain-crisis-k4e

VaR in practice:

Leveraging advanced data and analytics to anticipate supplier risk

Methodology:

value at risk (VaR) approach

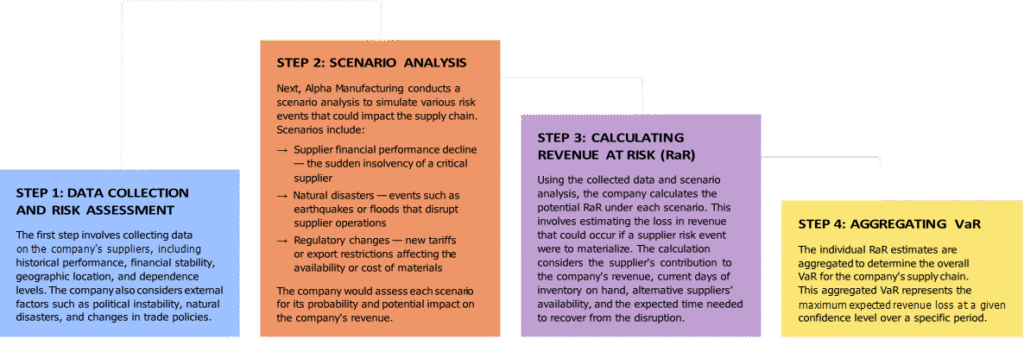

To quantify the potential revenue impact, Alpha Manufacturing employs the VaR methodology. In this case, the company uses it to estimate the revenue at risk due to supplier-related disruptions.

From data to decisions: why using value at risk calculations can bolster supply chain management 10

Conclusion

VaR is enabling supply chain teams to reliably assess

and prioritize risks, and to demonstrate financial value to their organization.

Value at risk has been a mainstay of financial analysis for decades and even permeated supply risk management for the best part of 20 years. However, what has changed

is threefold.

First, supply chain teams are increasingly considered a commercial arm of a business. Intrinsically, they are being asked to show their financial value to their management teams to secure budgets and resources.

Second, as global risks become more interconnected, supply chain issues become harder to anticipate. The resulting web means supply chain leaders must be clear on what risk types they’re protecting their supply chains from by employing mitigation strategies, which risk types to prioritize, and which to simply accept as unmitigated risks.

The third — and most crucial — value at risk has become more reliable thanks to the vast swaths of entity data at the supply chain team’s disposal.

At Moody’s, we believe the value at risk can empower supply chain leaders to communicate more effectively and transparently with board members

around supply chain decision-making. By incorporating VaR and making reliable calculations, we believe the VaR concept represents an effective and proven method that can be the North Star of any supply chain function, helping organizations build resilience and make better supply

chain decisions.

If you would like more information about incorporating value at risk into your functions or how Moody’s can support your journey toward supply chain resilience, please contact us.

© 2024 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY’S CREDIT RATINGS AFFILIATES ARE THEIR CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED OR OTHERWISE MADE AVAILABLE BY MOODY’S (COLLECTIVELY, “MATERIALS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEE APPLICABLE MOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’S CREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS,

NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S MATERIALS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S MATERIALS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND MATERIALS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND MATERIALS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND MATERIALS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES OR OTHERWISE MAKES

AVAILABLE ITS MATERIALS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND MATERIALS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR MATERIALS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT. FOR CLARITY, NO INFORMATION CONTAINED HEREIN MAY BE USED TO DEVELOP, IMPROVE, TRAIN OR RETRAIN ANY SOFTWARE PROGRAM OR DATABASE, INCLUDING, BUT NOT LIMITED TO, FOR ANY ARTIFICIAL INTELLIGENCE, MACHINE LEARNING OR NATURAL LANGUAGE PROCESSING SOFTWARE, ALGORITHM, METHODOLOGY AND/OR MODEL.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND MATERIALS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY’S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY’S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the credit rating process or in preparing its Materials.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond

the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDIT RATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service,

Inc. have, prior to assignment of any credit rating, agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it. MCO and Moody’s Investors Service also maintain policies and procedures to address the independence of Moody’s Investors Service credit ratings and credit rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold credit ratings from Moody’s Investors Service, Inc. and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Charter Documents – Director and Shareholder Affiliation Policy.”

Moody’s SF Japan K.K., Moody’s Local AR Agente de Calificación de Riesgo S.A., Moody’s Local BR Agência de Classificação de Risco LTDA, Moody’s Local MX S.A. de C.V, I.C.V., Moody’s Local PE Clasificadora de Riesgo S.A., and Moody’s Local PA Calificadora de Riesgo S.A. (collectively, the “Moody’s Non- NRSRO CRAs”) are all indirectly wholly-owned credit rating agency subsidiaries of MCO. None of the Moody’s Non-NRSRO CRAs is a Nationally Recognized Statistical Rating Organization.

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations

Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for India only: Moody’s credit ratings, Assessments, other opinions and Materials are not intended to be and shall not be relied upon or used by any users located in India in relation to securities listed or proposed to be listed on Indian stock exchanges.

Additional terms with respect to Second Party Opinions (as defined in Moody’s Investors Service Rating Symbols and Definitions): Please note that a Second Party Opinion (“SPO”) is not a “credit rating”. The issuance of SPOs is not a regulated activity in many jurisdictions, including Singapore. JAPAN: In Japan, development and provision of SPOs fall under the category of “Ancillary Businesses”, not “Credit Rating Business”, and are not subject to the regulations applicable to “Credit Rating Business” under the Financial Instruments and Exchange Act of Japan and its relevant regulation. PRC: Any SPO:

(1) does not constitute a PRC Green Bond Assessment as defined under any relevant PRC laws or regulations; (2) cannot be included in any registration statement, offering circular, prospectus or any other documents submitted to the PRC regulatory authorities or otherwise used to satisfy any PRC regulatory disclosure requirement; and (3) cannot be used within the PRC for any regulatory purpose or for any other purpose which is not permitted under relevant PRC laws or regulations. For the purposes of this disclaimer, “PRC” refers to the mainland of the People’s Republic of China, excluding Hong Kong, Macau and Taiwan.